How to get out of secured CCs???

<div class="user-question">How to get out of secured cards in credit?</div>

This guide is here to support you with the tools, knowledge, and confidence to take control of your credit and start building a brighter financial future - step by step, on your terms.

Let’s get into it.

Psst... to avoid this getting too long, we've decided to divide this into a three-part series. See our deep dive on credit repair services and what to do if your SSN has been stolen.

Don't have time for the whole thing? Here are our main takeaways.

<div class="frich-tip">1️⃣ The most important step towards getting out of secured CCs is improving your credit score. Here's our favorite tool that will help you achieve that - without any fees.</div>

<div class="frich-tip">2️⃣ If you're looking for more choice, explore our best credit repair tools.</div>

<div class="frich-tip">3️⃣ If you find yourself barely being able to make ends meet, here's an article we wrote about companies that give you free money.</div>

Don't like secured credit cards and want out?

Secured cards often don’t graduate to unsecured ones. Once your score improves, try applying for a starter unsecured card that has no annual fees or hidden costs.

Secured cards are great to start building credit, but:

- Your deposit is locked up

- They often come with low limits and no rewards

- Many don’t graduate to unsecured cards

<div class="frich-tip">Frich tip: currently in the process of building your credit? Fizz is our team’s favorite tool that will help you build credit without any interest rates, late fees, credit checks, or minimum deposits to worry about! </div>

Steps to transition successfully

1️⃣ Build a track record

- Use 10–30% of your limit.

- Always pay in full, on time.

2️⃣ Ask if your issuer offers graduation

- Some cards (like Capital One Secured or Discover it® Secured) automatically review your account after 6–12 months.

<div class="frich-tip">Frich tip: if you're currently looking to get a secured credit card, here are our favorite options.</div>

3️⃣ Apply for a starter unsecured card

- Choose one with no annual fee.

- Use it responsibly - keep both open initially to help your credit age and utilization ratio.

<div class="frich-tip">Frich tip: here are our favorite options for the best no-annual-fee credit cards!</div>

4️⃣ Get your deposit back

- Once you’re approved for an unsecured card and no longer need the secured one, close it only if it won’t harm your credit utilization or age significantly.

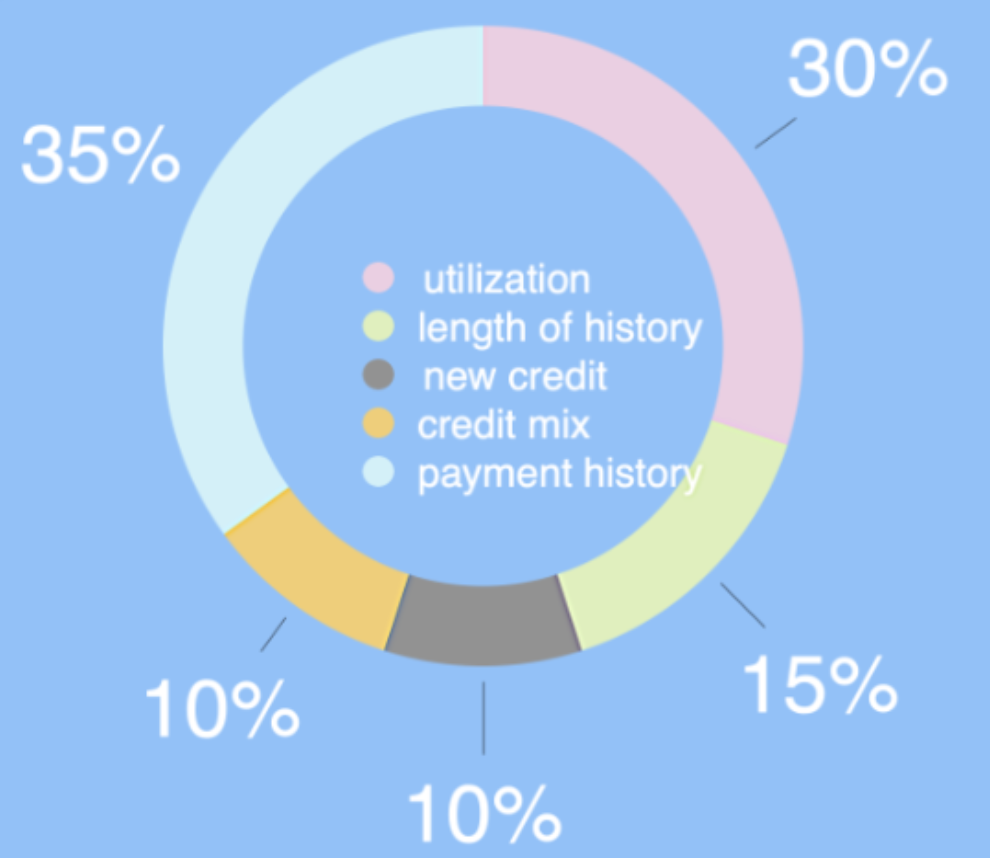

What to know about credit cards and utilization

Credit cards are one of the biggest drivers of your credit score, but also the easiest way to get into trouble.

- Your credit utilization ratio - the amount you owe compared to your total credit limit - has a significant impact.

- Utilization rates under 30% are good, but under 10% are ideal. If your limit is $1,000, avoid exceeding $100 in revolving debt.

- If you're carrying a balance, paying it down can significantly boost your score.

<div class="frich-tip">Frich tip: If you've already found yourself in a situation where you've accumulated debt across multiple cards, take a look at these companies that can help you deal with your existing debt.</div>

You got this! -- Gwyneth