How to avoid paying credit card interest & fees

In this article:

- How to figure out your credit card fees

- How to avoid paying any fees & interest

- How to strategically plan your purchases to give you the most time to pay back

When you pay with your credit card, you’re not technically paying with your own money. You’re borrowing from your bank (e.g. Chase, Citi, Bank of America) and then paying them back. If you don’t pay everything back on time, you get charged interest. Interest varies from account to account based on how good your credit score is.

So treat it like that = you’ve borrowed money with a concrete due date. After that, you’re paying back more than you spent (which obviously you wouldn’t want).

Let’s break down how to read your credit card statement:

When you open up a credit card, you get assigned a statement close date. Check your credit card portal to see what the date is & put it in your calendar. You can also always reach out to your bank, and ask to move the date to be right after your paycheck hits to make sure you always have the funds to pay off your bill.

Taken from the credit card statement of one of our team members (🤫), you can see that the closing date is October 17. What does that mean? I am responsible for transactions made between September 18 to October 17.

From the screenshot, you can see that I have to pay latest by November 12 (the payment due date). So rough math - this credit card’s grace period to pay the bill is 26 days. This means that tI won’t be paying any fees or interest on charges made between 09/18-10/17 until 11/12. Long story short - I have 26 extra days to pay back the bank what I owe. After that they start charging me extra. Each bank has a slightly different grace period, but it’s usually around 20ish days.

Okay so what’s the minimum payment? It’s the fee that I must pay before your payment due date to avoid getting hit with an additional fee. The fee is usually around $30-40, however it changes card by card. Here you can see that my late fee is up to $40 (the same as my minimum payment).

BUT - if I only pay the minimum payment, I will still be hit with interest rate for the remaining amount. In this case, $1,339.20-$40 =$1,299.20. This amount will be hit with the interest rate defined by my card (again, this varies based on the card and credit score). For me, my interest rate (APR) is 27.99%.

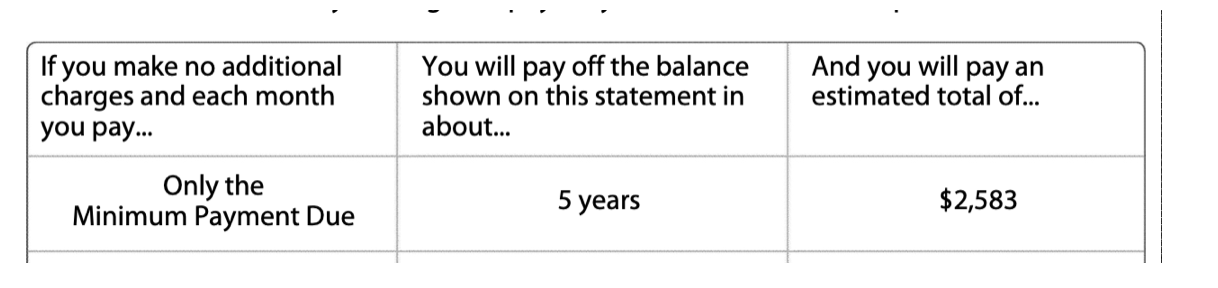

The credit card statement actually does a good job showing what would it look like if I only paid the minimum payment due.

So I spent $1,339.20 between 09/18-10/17. If I paid $40 (my minimum payment) every month & never bought anything else, it would take me 5 years and an extra $1,243.80 to pay this off. So that’s basically double the amount compared to what I borrowed. This is what the 27.99% APR does to my balance.

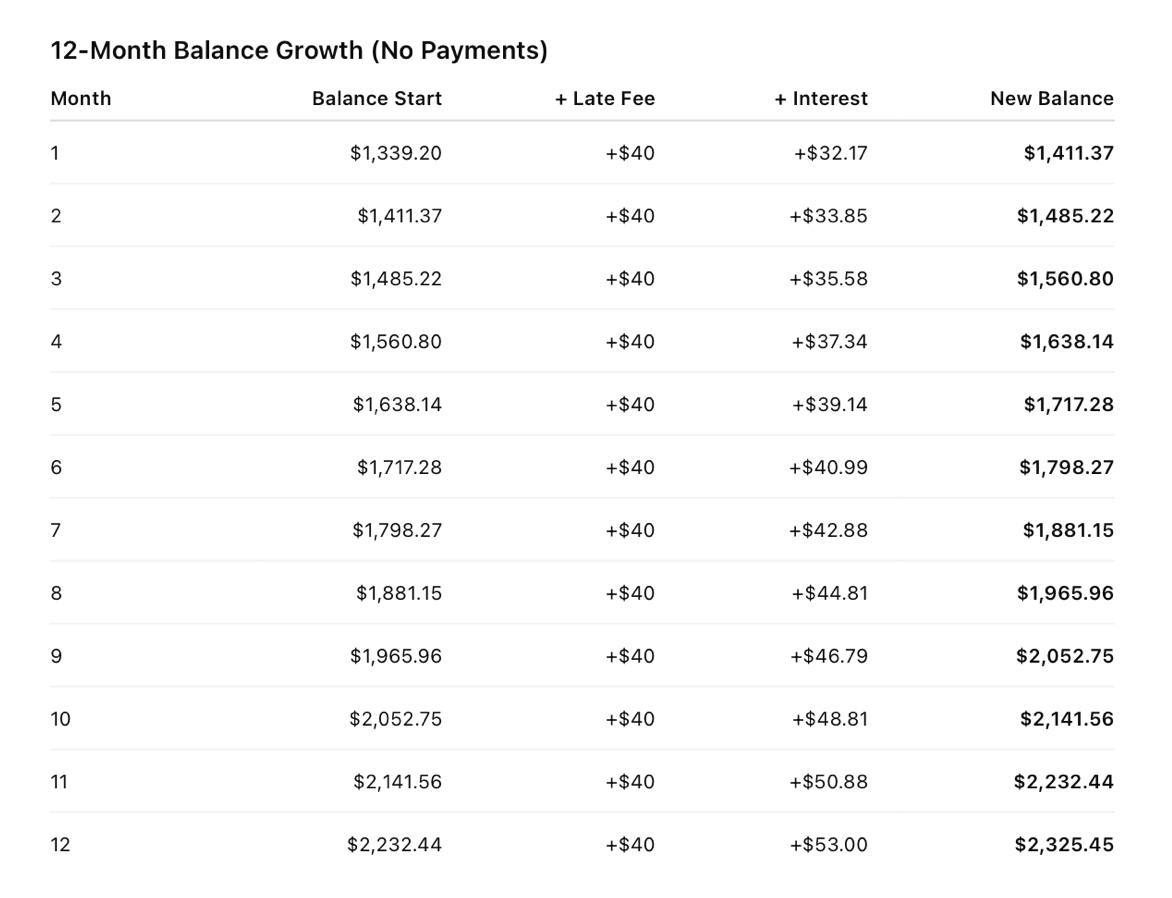

What does that for me in the short term? Let’s assume I have a really rough year and I can’t make any payments on this card. Here’s what that will cost me:

So each month, I’ll be paying a $40 fee, interest on my updated balance, and interest on the $40 fee. This is how my balance snowballs and one year later $1,339.20 turns into $2,325.45. My debt has now grown by $986.25 just from interest and fees.

Recapping based on my account:

Billing cycle: 09/18-10/17

Statement close date: 10/17

Grace period: 10/17-11/12 (26 days)

Due date: 11/12

Minimum payment: $40

Minimum payment late fee: up to $40

APR: 27.99%

Here are our credit card best practices:

- Call your bank and ask to move your statement close date a few days after your payday so you can comfortably pay your bill in full & avoid confusion on how much you’ve spent

- Set up autopay for that day to automatically pay the whole bill

- Treat your credit card as a debit card - never buy more than you can afford to pay off within a month

- Never, NEVER miss to pay at least your minimum payment due. If you don’t feel comfortable setting autopay for the full balance, set it for at least the minimum payment due.

- Bonus tip: if you have a large expense, charge it the day after your billing cycle ends. For me it would be the 18th. This would give me roughly 55 days (29 days until close date + 26 day grace period) to pay this back. On the contrary, if I made a purchase on the 16th, I would have to pay in 27 days (1 day until close date + 26 day grace period).