EOY Tax Moves

<div class="user-question">Hi Frich! I’m currently at university, and even though I haven’t really had a real income yet, I’m already a bit confused and nervous about taxes since no one teaches us about it in school. I’ve seen online a lot about tax exemptions and ways to write stuff off, but I’m not sure if that’s even true. So my question is—how do you even file taxes? And what are some of the main things to keep in mind to decrease the amount of taxes I pay?</div>

Hi, I’m Daniel, the founder and CEO of Fifr, the financial wellness platform built for everyone. Personal finance is more than a job - for me it’s deeply personal. So let’s tackle taxes and make them less scary for you ⬇️

🏛️ Taxes: you’re not alone - they are confusing

Let’s be real - taxes can be overwhelming, and there’s a lot of bad advice floating around online.

<div class="frich-tip">Frich tip: Don’t take advice from unvetted people on TikTok. It’s often fraud and could get you in serious trouble!</div>

The good news? Most people don’t need to worry too much about “write-offs.” Instead, you want to focus on tax-advantaged accounts, which are powerful tools to minimize the taxes you pay over your lifetime. These strategies don’t only save you money now - they can also set you up for long-term success.

Let’s dive into some smart tax moves you can make before the year ends.

🏛️ Smart tax moves to make before filing your taxes

First, it's important to remember that many tax advantages often have expiration dates on them.

If you live in a high-tax state like New York or California, making these types of tax moves can be especially impactful. Additionally, the earlier you start, the more you stand to gain.

1️⃣ Make retirement contributions

Retirement savings might not be on your radar yet, but trust me, starting early can be a game-changer AND it decreases the taxes you end up paying. And you don’t necessarily have to wait until retirement age to access those savings 👀

- 🏛️ 401(k): A retirement account offered by employers where you can contribute pre-tax dollars (reducing your taxable income) or post-tax dollars to grow tax-free for your retirement.

- 🏛️What to know: If you have extra cash, you should try to contribute as much as possible before year-end, up to $23,500 in 2025.

- 🏛️ IRA: An individual retirement account you open on your own with similar tax benefits to a 401(k).

<div class="frich-tip">Frich tip: one of our favorite personal finance YouTubers, Graham Stephan, dives more into 401(k)s and IRAs here.</div>

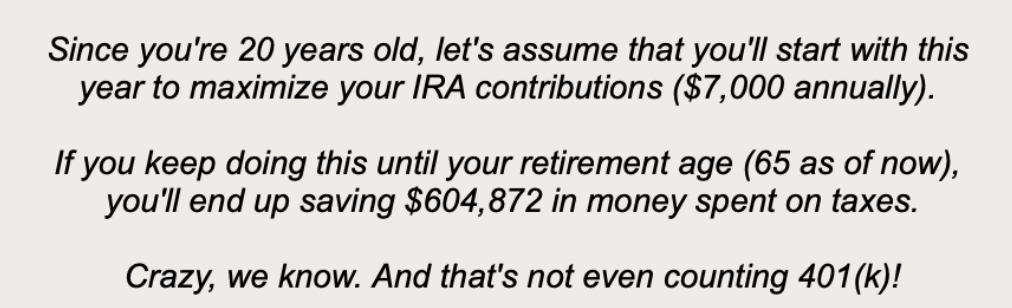

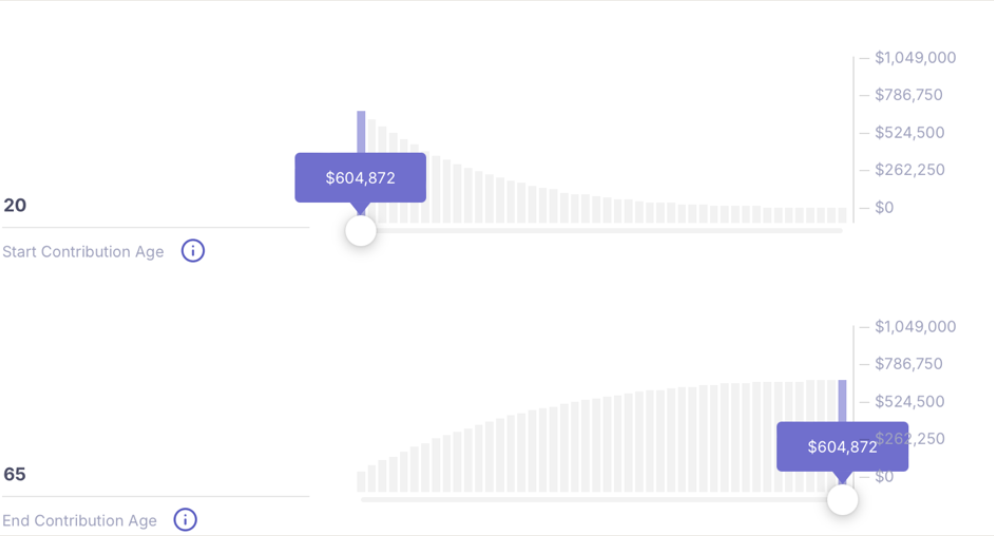

- 🏛️ What to know: If you don’t have a 401(k) (which you wouldn't have until you're employed), consider opening an IRA. You can contribute up to $7,000 for 2025, and they also come in two options, traditional and Roth.

<div class="frich-tip">Frich tip: Check out this calculator that can help you visualize how much tax savings IRAs can generate over your lifetime!</div>

2️⃣ Contribute to Health Savings Accounts (HSAs)

An HSA isn’t just for medical bills—it’s one of the most powerful tax-advantaged accounts out there, offering triple tax benefits:

- 🏛️ Contributions are tax-deductible, meaning they reduce your yearly taxable income

- 🏛️ Investment gains are tax-free, meaning you don't pay taxes on the money you make off your investments

- 🏛️ Withdrawals for qualified medical expenses are tax-free as well

If you have a high-deductible health plan, look into topping up your HSA before the year ends.

3️⃣ Use your Flexible Spending Account (FSA)

FSAs are another great tool that decrease your total tax bill, but there’s a catch: many FSAs have a “use-it-or-lose-it” policy.

<div class="frich-tip">Frich tip: Remember that if you have money in your FSA, you must spend it before the year ends. Otherwise, it’s gone. Panicking to find what to buy? GlassesUSA.com accepts FSA (and HSA) funds for thousands of prescription sunglasses, glasses and contact lenses. Psst...subscribe at GlassesUSA.com and get 50% off your first purchase. 🎁</div>

🌟 Pro Tip: Start small, but start now

Even if you can’t max out these accounts, putting something away is better than nothing. Small contributions now mean big savings (and less tax stress) later. Not sure where to stash your cash while you learn the ropes? A high-yield savings account is a simple way to grow your money passively while keeping it accessible. And if you're left feeling like you want to learn more, here are some of our personal favorite finance YouTubers:

🌟 Graham Stephan - entertaining, clear personal finance guidance

🌟 Mr. Money Mustache - practical finance and life advice

🏛️ When you’ll need to worry about personal taxes

Right now, taxes might not be a big concern if you don’t have an income. But as soon as you start earning, here’s what you need to know.

Tax filing timeline

- 📆 The official tax-filing deadline is typically April 15 each year.

- 📆 Start preparing your documents in January to avoid last-minute stress.

What you’ll need to file

- 📆 W-2s: Provided by your employer, detailing your earnings and tax withholdings.

- 📆 1099s: For freelance or gig income work, you’ll receive these instead of W-2s.

- 📆 Receipts: For deductible expenses like education costs or medical bills.

Found this valuable? Here are some more deep dives from the Frich team 🤝

✅ 7 tax strategies that can save you up to $50K before the year ends

✅ What happens with your health insurance when you get laid off?

✅ Here's your guide to reviewing 2025

We covered a lot today, and I get it - taxes can feel overwhelming. But trust me, making smart tax moves now can significantly reduce your tax burden and set you up for long-term financial success. By starting early and staying proactive, you can build strong financial habits that make taxes feel less intimidating and more manageable over time.

The path to financial independence begins with small, intentional steps. And the good news? You don’t have to do it alone. Fifr is here to help. It’s the resource I wish I had when I was 19 and suddenly faced massive debt and had a million questions on how to begin thinking through my finances.

Happy saving,

Daniel

CEO, Fifr