Is renting a waste of money? [PT 2/2]

<div class="user-question">How do I know that it’s time to stop renting and it makes financial sense to buy a place? And how do I prepare for this?</div>

Note: to avoid this getting too long, we've split up this deep dive into two emails. Here's the first half!

I’m Benjamin - I’ve had the privilege of coaching many first-time buyers through this decision-making process, and I built Fincast to make mortgages more manageable and savings more accessible. Let’s walk through how to know if you’re ready, when you’re ready, and the exact steps you can take to be more prepared and less overwhelmed.

If you’re ready - here’s exactly how to prepare

1️⃣ Fine-tune your credit

- On-time autopay on every bill

- Pay down revolving card balances (aim <30% utilization; <10% is great)

- Pause new credit (including “buy now, pay later”) in the months before applying

<div class="frich-tip">Frich tip: Check your credit score for free here!</div>

2️⃣ Build a true home fund. Beyond your down payment, save for:

- Closing costs (2-5%): it’s best to prepare for worst-case scenarios when it comes to cost planning

- Moving + set-up: movers, deep clean, locks, blinds, small furnishings, paint

- Maintenance reserve: start that 1% / year plan now so day-one ownership isn’t a shock

<div class="frich-tip">Frich tip: Keep this money in a HYSA so it grows for free! Here is our team's favorite option.</div>

3️⃣ Get pre-approved (not just pre-qualified). Pre-approval = the lender actually reviewed your docs and told you a real buying power number. That protects your time, helps your agent, and strengthens offers.

4️⃣ Shop for a home (and make an offer!). Once you’re pre-approved, get with your real estate agent and look at homes within your budget. Use that pre-approval letter to show sellers that you’re a serious buyer. When you find your dream house, make a competitive offer.

5️⃣ Apply for the loan. The pre-approval was just an estimate of what you could afford. Now it’s time to apply for the actual mortgage and see what the real numbers look like. Send them your signed purchase contract, and within three business days, they must send you a Loan Estimate. This is your secret weapon when making sure you don’t overpay.

6️⃣ Shop your Loan Estimate (this is the cheat code). Even loan officers shop their own mortgages. Why? Because two lenders can review the same borrower and offer totally different deals. Here’s a cheat sheet on the most important factors to compare on the Loan Estimate:

- APR - the all-in cost, not just the rate

- Points - fees that “buy down” the rate

- Lender credits - they can reduce your closing costs

- Rate options - show me zero-point, 1-point, and 2-point scenarios

- Temporary buydowns - useful if cash is tight the first 1-2 years

- Lock timing & extension policy - so you’re not surprised

<div class="frich-tip">Frich tip: There are thousands of lenders who want to do your loan. Make them compete for it. Don’t feel obligated to use your parents’ banker. Loyalty is great for friends - not always for financing. That’s exactly why I built Fincast - to make lenders compete for you.</div>

The “don’t do this during underwriting” list

❌ Don’t change jobs or employment type mid-process.

❌ Don’t finance a car or open new credit lines.

❌ Don’t make large unexplained bank transfers.

❌ Don’t co-sign anything.

These can all delay or derail approval. Lock in the house first; then grab the new car.

Know your numbers

1️⃣ Down payment

- Reality: First-time buyers often put well under 20% down.

- Trade-off: Smaller down payments add PMI (mortgage insurance). It’s not the end of the world - just a line item.

<div class="frich-tip">Frich tip: Keep this money in a HYSA so it grows for free! Here is our team's favorite option.</div>

2️⃣ Debt-to-Income (DTI) = your monthly debt payments (cards, student loans, car, plus the new housing payment) divided by your gross monthly income.

- Many approvals are comfortable when total DTI ≤ 43-45% (programs vary).

<div class="frich-tip">Frich tip: That’s a ceiling, not a goal. Pick a payment that leaves you breathing room for life. If the all-in homeowner number lands between target and max and you still hit savings goals, you’re aligned.</div>

3️⃣ Your Personal Payment Comfort Zone. Create two numbers:

- Target payment you’d be happy to pay every month

- Max payment you could handle without stress if costs shift

Practical & emotional check

- Lifestyle mapping: From a target address, map your commute, gym, grocery, pet care, weekend spots. Does the map look like a life you want daily?

- Neighborhood vibe audit: Visit day and night. Are people out? Do neighbors care for their places? Do you feel good walking the block?

- Stage-fit: Pets, kids, roommates, remote work - does the home support that?

- Love it enough? You don’t need a perfect home, but you should like it enough to care for it - because you’re responsible now, not a landlord.

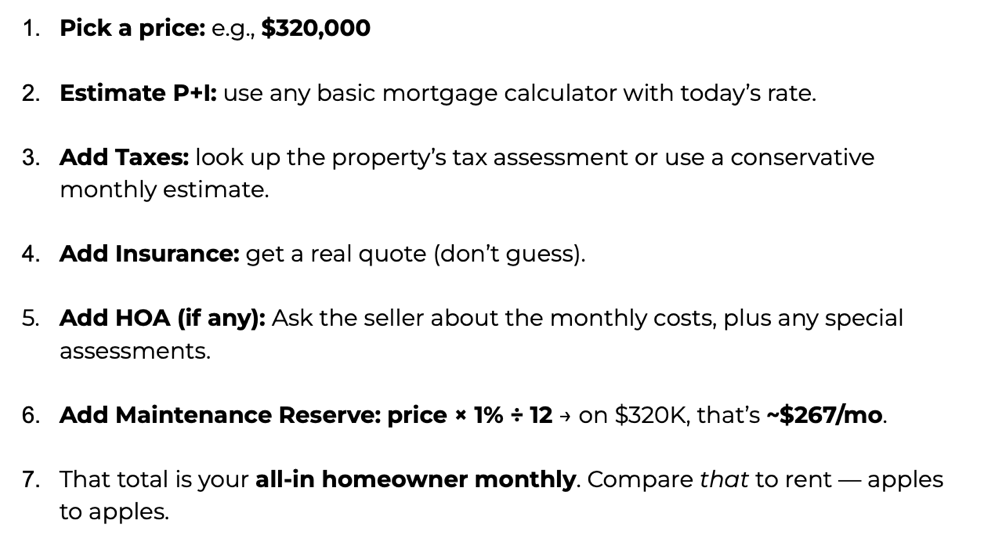

Quick mini-math you can personalize

Use this like a template - plug in your numbers:

Homeownership can be a great long-term wealth builder - but timing matters. Make the move when the payment works, the place fits, and your life is ready for the commitment.

Buy when the payment and the place both fit your life - not because someone else says you “should.”

<div class="frich-tip">Frich tip: Until then, use renting strategically: build credit, stack cash, explore neighborhoods, and keep your options open. You’ll feel it when it clicks.</div>

Tiny glossary

Quick checklist

Found this valuable? Here are some more deep dives from the Frich team 🤝

✅ Groceries, Gas, Gifts - Everything’s Up… Except Your Paycheck

✅ Can I trust credit repair services?

✅ Will I ever be able to buy a home??

Good luck! Hope this was helpful.

Benjamin Schieken, Founder & CEO of Fincast